NEW DELHI: According to a telecom sector report from Motilal Oswal Financial Services, discussion with with industry experts indicate that a price hike could be around the corner and may be anticipated soon as economic activity has restarted post the COVID-led lockdown and demand for data consumption is growing unabated.

The timing of a price hike is in line with our expectations of a tariff hike by FY21-end or early FY22.

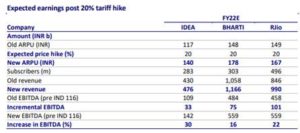

A 20% price hike should increase Airtel, AReliance Jio, VodafoneIdea’s ARPU to Rs 178, Rs 167, Rs 140 in FY22. At 70% incremental margin, EBITDA (pre IND AS 116) in FY22 should touch Rs 559b, Rs 559b, Rs 142b, a 16%/22%/30% increase at the consolidated level. MOFS has not factored in a material price hike in the model at present. Without any tariff hike, Motilal Oswal Financial Services expects Airtel /RJio to generate post interest FCF of Rs 64b, Rs 64b, including one-time spectrum renewal cost of Rs 130b, Rs 280b.

A 20% price hike should increase Airtel, AReliance Jio, VodafoneIdea’s ARPU to Rs 178, Rs 167, Rs 140 in FY22. At 70% incremental margin, EBITDA (pre IND AS 116) in FY22 should touch Rs 559b, Rs 559b, Rs 142b, a 16%/22%/30% increase at the consolidated level. MOFS has not factored in a material price hike in the model at present. Without any tariff hike, Motilal Oswal Financial Services expects Airtel /RJio to generate post interest FCF of Rs 64b, Rs 64b, including one-time spectrum renewal cost of Rs 130b, Rs 280b.

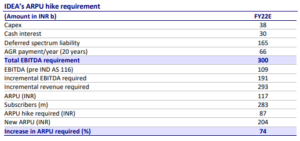

Although this should provide IDEA with additional cash flow, it would still not be enough to fulfill its obligations. Our workings suggest that IDEA needs 74% ARPU hike to achieve EBITDA (pre IND AS 116) of Rs 300b to sufficiently furnish its complete cash obligations sustainably in FY23, including deferred spectrum payments. It also needs to arrest its subscriber churn to realize the benefit of price hike. As we witnessed in the previous round of price hike (Dec’19), ~25% tariff hike increased its EBITDA by just INR14b (25%), given the huge subscriber churn. This was a far cry from our anticipated EBITDA increase of Rs 43b.

Motilal Oswal Financial Services continues to remain bullish on Airtel and Reliance Jio with a target price of Rs 650, Rs 900 (for its 66% stake). Motilal Oswal Financial Services has assigned a higher multiple of 11x/18x to Airtel, Jio for capturing expected gains from any potential tariff hike, higher market share gains.

Motilal Oswal Financial Services continues to remain bullish on Airtel and Reliance Jio with a target price of Rs 650, Rs 900 (for its 66% stake). Motilal Oswal Financial Services has assigned a higher multiple of 11x/18x to Airtel, Jio for capturing expected gains from any potential tariff hike, higher market share gains.

The premium valuation toJio captures the additional a) Digital revenue opportunity, and b) growing subscriber market share in the low-cost device market. Motilal Oswal Financial Services continue to maintain IDEA under review due to its liquidity crunch and limited clarity on business continuity.